The World Before the Fortune

Industrial Britain already depended on movement — coal, manufactured goods, and the slow grind of canal barges and horse-drawn wagons. The country was wealthy but bottlenecked. Distance was expensive, and every manufacturer who wanted to ship further paid dearly for the privilege. Into this environment arrived the railway, promising to collapse time and distance together into something that had never quite existed before.

Power in that world did not belong only to the loudest promoter or the most visible asset. It belonged to whoever understood how capital, access, timing, and physical infrastructure could be arranged into a machine that would keep producing advantage long after the initial investment was made. For Hidden Fortunes readers, this is the context that makes Railway Mania interesting beyond the spectacle of a bubble. It is a story about how wealth compounds once someone begins controlling the structure that everybody else still needs.

The Rise

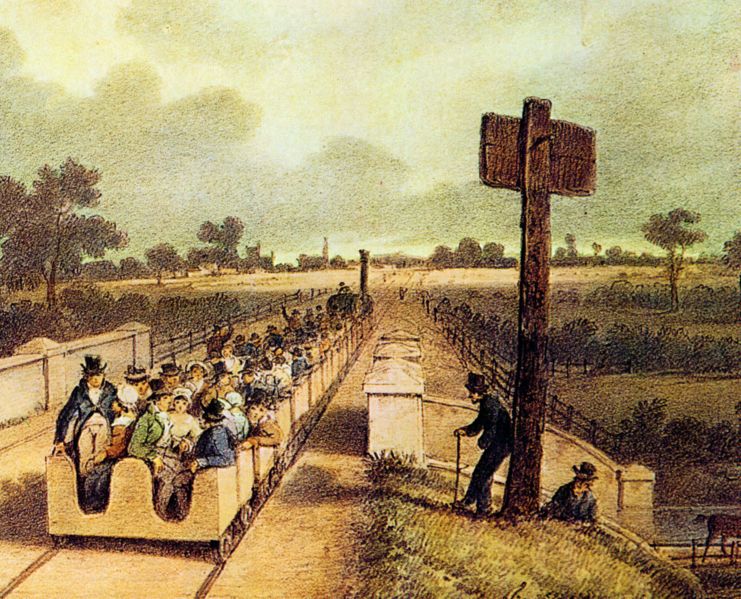

Speculators poured money into railway schemes because they believed they were buying proximity to the transport spine of a new economy. The Liverpool and Manchester Railway had opened in 1830 and proved the technology worked. By the early 1840s, a new wave of promoters arrived with parliamentary bills, prospectuses, and promises of returns that seemed almost too certain to question. George Hudson — the “Railway King” — became the most prominent figure of the mania, assembling a web of companies and paying dividends out of fresh capital to sustain confidence in lines that had not yet turned profitable.

The same dynamic that inflated tulip prices in Amsterdam and the South Sea Company in London was operating here, but with a critical difference: the underlying asset was real. Railroads would eventually move millions of passengers and vast tonnages of freight. That kernel of genuine utility made it easier for optimism to outrun discipline. Investors were not simply chasing air — they were chasing something that looked, reasonably enough, like the future.

The Expansion of Power

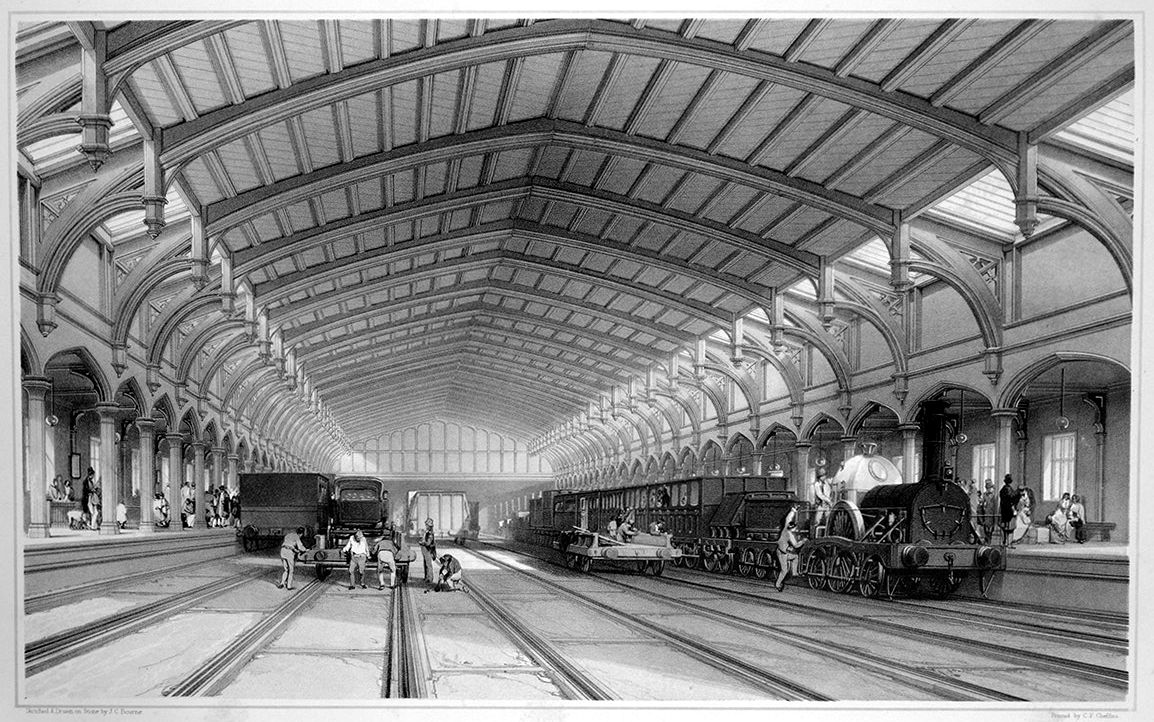

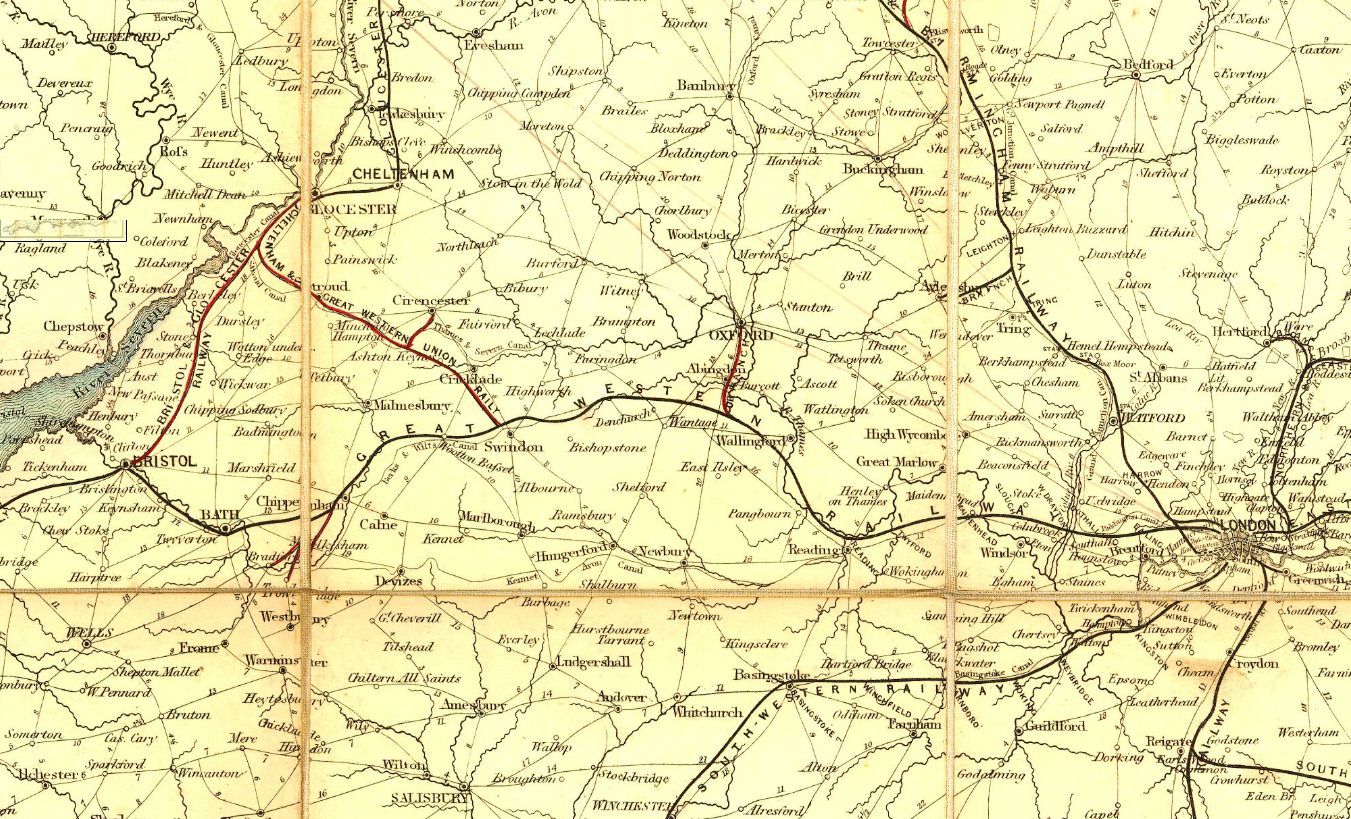

By the mid-1840s, Parliament was authorizing hundreds of new railway schemes per session. Engineers were surveying lines across England, Wales, and Scotland. The Great Western Railway under Isambard Kingdom Brunel pushed westward toward Bristol and beyond. The Midland Railway began knitting together the industrial heartland. Capital rushed toward iron and timber and earthworks on a scale that no previous infrastructure project in British history had attempted.

What made this expansion strategically powerful was not the individual lines but the emerging network. Once a city was connected, the cost of not being connected rose for every city still outside the system. Vanderbilt would later use precisely this logic in America — control the chokepoints and the network rewards your position automatically. In Britain during the 1840s, the same principle was already operating, even if most investors were too focused on share prices to see it clearly.

The Hidden Strategy Behind the Fortune

The hidden strategy behind Railway Mania was not simply speculation — it was the realization, grasped most clearly by the engineers and the most sophisticated promoters, that overfinancing an infrastructure system could still leave behind a skeleton that future operators would inherit for free. Lines built in the mania at prices that could never deliver adequate returns on their capital cost would nonetheless move trains. The underlying asset could not be uninvested.

This is what separates Railway Mania from a pure financial bubble. The Panama Canal syndicate destroyed fortunes and left an uncompleted ditch. Railway Mania destroyed fortunes and left a national rail network. The wreckage was productive. For later investors who bought bankrupt railway bonds at pennies on the pound, the collapse was not a tragedy but an opportunity — the same infrastructure at a fraction of the original cost, with all the traffic still flowing through it.

The Cost, Risk, or Collapse

Investors lost money on a massive scale. Thousands of middle-class families who had committed their savings to railway shares watched their capital evaporate when the mania broke in 1847 and 1848. George Hudson’s empire unraveled under allegations of fraud and financial manipulation. Parliamentary inquiries exposed how dividends had been falsified and capital misappropriated. The Railway King ended his career in disgrace and died effectively ruined.

But the physical infrastructure survived. Lines that had been overbuilt and underpriced for their original investors were reorganized, amalgamated, and made to work under new ownership. The Midland Railway, the Great Northern, the London and North Western — the companies that emerged from the wreckage of the mania became some of the most powerful industrial organizations Britain had ever seen. The bubble had allocated capital badly, but the capital itself had not vanished. It had been converted into something that could not be undone.

Lessons for Modern Business Readers

1. Control the hidden layer

The most durable advantages in Railway Mania did not come from owning the most shares. They came from controlling the physical layer — the track, the bridges, the terminals — that everyone else needed to operate. Once that layer was in place, it collected tolls from every competitor and every customer who passed through it.

2. Dependency compounds faster than attention

The strongest railway networks did not only attract investment. They made other businesses — manufacturers, merchants, coal mines, cattle markets — depend on terms they did not design and could not easily renegotiate. That structural dependency outlasted the mania and made railways more powerful after the bubble than during it.

3. Infrastructure is often the real moat

The quiet layer beneath the product or headline usually produces the most durable advantage. Railway promoters sold excitement and returns. What they were actually building was a physical moat — one that no competitor could easily replicate once the geography had been claimed.

4. Bubbles can be productive

Not every bubble destroys what it funds. Railway Mania is one of the clearest historical examples of speculative capital building something real. Modern parallels are not hard to find: the dot-com bubble overfinanced fiber-optic infrastructure that later powered the internet economy at a fraction of its original cost.

5. The collapse is often the best entry point

The investors who made fortunes from British railways were rarely those who bought during the mania. They were the ones who bought the reorganized companies after the crash — acquiring the same infrastructure at a discount deep enough to make the economics finally work.

6. Reader trust comes from mechanism, not myth

Hidden Fortunes wins when it explains how power worked rather than flattening it into legend or outrage. Railway Mania is not a story about greedy investors getting what they deserved. It is a story about how speculative capital, even when catastrophically misallocated, can leave behind structural advantages that outlast the original mistake.

Read Next

For readers who want to go deeper into how financial manias work — and how Railway Mania fits into a broader pattern of credit-driven infrastructure speculation — the essential next step is Charles Kindleberger’s Manias, Panics, and Crashes. It is the clearest analytical framework available for understanding why rational-seeming investors consistently overshoot, and why the infrastructure left behind so often outlasts the capital that built it.