The South Sea Bubble is often remembered as a cautionary tale about greed and madness. That is true, but incomplete. Bubbles this large are rarely built on public foolishness alone. They usually require a mechanism that looks respectable enough for intelligent people to trust before it becomes absurd enough for everyone else to chase.

In Britain, that mechanism was government debt wrapped in political credibility. The South Sea Company did not need a thriving real business to ignite mania. It needed enough proximity to the state, enough financial engineering, and enough rising prices to convince investors that paper could keep outrunning substance.

That is why this is a Hidden Fortunes story. The hidden strategy was not the trade dream. It was turning official credibility into speculative fuel.

The World Before the Fortune

Britain entered the South Sea story with a major fiscal problem. War had left the state carrying significant debt, and managing that burden created opportunities for financial innovation, favoritism, and opportunism. Debt itself was not the scandal. The scandal lay in what people did with the authority to reorganize it.

This is a critical starting point because the bubble did not emerge from nowhere. It emerged from a real structural need: the state wanted solutions, investors wanted returns, and politically connected operators saw a chance to sit between public finance and private gain.

That combination is combustible. When a company can present itself as a remedy to a government problem, it can borrow some of the government’s credibility even if its own underlying economics are weak.

What matters for modern readers is that the early advantage rarely looks glamorous. In every era, the future fortune begins inside disorder, partial information, and assets that seem too dull for the headline economy. The winner is usually the operator who sees which hidden layer will still matter after the visible excitement burns off.

The Rise

The South Sea Company began as a trading and finance company, but its eventual power came far less from trade than from debt conversion. The promise that it might profit from access to Spanish America helped create glamour, yet the deeper business case increasingly depended on how it interacted with public obligations and market psychology.

Political support mattered enormously. Royal association and parliamentary backing gave the enterprise a legitimacy halo, and investors treated that halo as if it were a substitute for hard commercial proof. This is one of the oldest mistakes in capital markets: confusing political proximity with productive durability.

Once the company was accepted as a vehicle for taking over large portions of national debt, the stage was set for the share price itself to become the engine of wealth. Investors were no longer buying only a business story. They were buying rising confidence.

The temptation in stories like this is to make the rise look automatic once the first decisive move is made. History is harsher than that. The rise matters because it shows a sequence of disciplined choices, each one widening the moat until rivals start confusing deliberate structure with inevitability.

The Expansion of Power

The mania expanded because the market started feeding on its own motion. Rising prices appeared to confirm the brilliance of the scheme. More investors rushed in. Promoters multiplied. Other speculative ventures tried to surf the same tide. The entire environment became an amplifier for paper credibility.

This is where the bubble becomes especially relevant to modern readers. Financial engineering can be powerful, but when its success depends too heavily on ever-rising valuations, the line between mechanism and mirage gets thin. The South Sea machine was strongest when people stopped asking what durable cash flow sat underneath the enthusiasm.

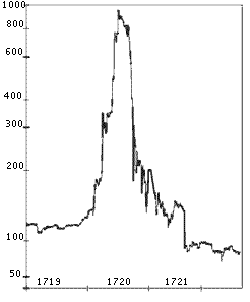

By the summer of 1720, the share-price ascent itself had become the story. That is a dangerous stage in any market, because once price becomes proof, skepticism looks irrational right up until collapse makes skepticism obvious again.

From an American business perspective, this is where the story becomes more than history. Expansion at this level is never just hustle. It is the conversion of one good position into a reinforcing network of positions, so that the system itself becomes harder to challenge than any single product, trade, or asset inside it.

The Hidden Strategy Behind the Fortune

.jpg)

The hidden strategy behind the fortune was the monetization of state credibility. The company took something the public viewed as solid — government obligation, political backing, and the aura of official approval — and converted it into speculative demand for its own shares.

That distinction matters. The bubble was not simply about dreamers imagining trade riches. It was about a structure that let insiders and early participants benefit from rising prices while the broader market treated the state-linked story as a substitute for discipline. The product increasingly became momentum itself.

This is why the South Sea Bubble deserves to be studied as a debt machine before it is studied as a mania. The share-price explosion was the visible frenzy. The hidden mechanism was the way debt restructuring, political access, and credibility transfer created the conditions in which frenzy could scale.

For modern readers, the business lesson is severe: when an asset derives too much of its value from institutional aura, policy intimacy, or a reflexive price loop — rather than durable economic output — the risk is often much larger than the public narrative admits.

The premium lesson is restraint. Great fortunes often look dramatic from the outside, but internally they are usually built on cold sequencing. One advantage leads to another. One layer of control finances the next layer of control. The people who build enduring wealth are often the people who understand that timing, structure, and recurring leverage matter more than theatrical motion.

What makes the South Sea story premium rather than generic is that the bubble had institutional teeth. This was not a fringe frenzy. It was a market event energized by official proximity, and that made the illusion stronger for longer than a purely private fantasy could have managed.

That distinction is what keeps the episode modern. Investors are always more vulnerable when they believe not only in an asset but in the aura around the asset. If official endorsement, elite participation, or regulatory intimacy begins to feel like a substitute for cash flow, the market can rise much farther than sober arithmetic would justify. The collapse then feels like a shock, even though the hidden weakness had been present all along.

In that sense, the bubble was not just a story about greed. It was a story about how institutional theater can postpone skepticism until skepticism becomes expensive to rediscover.

The key strategic insight is that credibility itself can become a temporary asset class. Once traders begin buying the aura around power rather than the economics beneath it, speculation gains a second engine and becomes far harder to stop.

That is why the episode still reads like a warning to modern markets built on narrative surplus and political intimacy.

When confidence and official aura start trading like assets, correction usually arrives late and violently. The South Sea machine proved exactly that.

The Cost, Risk, or Decline

The collapse, when it came, was devastating. Investors were ruined, scandal spread through the political class, and official inquiries exposed bribery, self-dealing, and elite speculation. Confidence that had seemed almost sovereign suddenly looked paper-thin.

The scandal also produced a political lesson that has never gone away. When governments and markets become too entangled through opaque favoritism, the resulting wealth can be real for a time and still structurally rotten underneath.

That darker edge should not be treated as a footnote. It is part of the real anatomy of power. Many wealth systems become most impressive at the exact moment they are also becoming morally brittle, politically exposed, or structurally overconfident. Hidden Fortunes works only when the strategy remains visible without pretending the costs were imaginary.

Lessons for Modern Business Readers

1. Political credibility can inflate prices without improving fundamentals

A state-linked halo can make a weak structure look stronger than it is.

2. Debt engineering can become a speculative product

The South Sea story shows how a financial solution can turn into a mania once rising prices become the real attraction.

3. Price momentum is not the same as productive value

The market often learns this distinction late and painfully.

4. Elite participation does not guarantee quality

In many bubbles, insider proximity helps attract capital before it protects the public.

5. Reflexive markets punish complacency

Once price becomes proof, the reversal can be violent because confidence had been doing too much of the work.

6. Follow the mechanism, not just the mood

A bubble becomes easier to understand when you ask what hidden structure is feeding the enthusiasm.

The darker lesson underneath all of this is that fortune rarely comes from surface activity alone. In almost every era, the decisive wealth goes to the people who control the terms, not just the transaction. Hidden Fortunes exists to make that layer visible, and this story does exactly that.

For founders, investors, and operators in the United States and other English-speaking markets, the practical value of this history is not imitation at the surface level. It is pattern recognition. Every modern industry has its own version of routes, chokepoints, permissions, and recurring flows. The challenge is to identify them early, reach them before the market fully prices them in, and build enough discipline around them that success compounds instead of dispersing.

Book Recommendation

For readers who want the best next step, start with The South Sea Bubble by John Carswell. It is the right Amazon follow-up for this topic because it gives the wider historical context behind the fortune, the machinery of power, and the strategic logic that made the story endure.