Affiliate Disclosure: This post contains affiliate links. If you click through and make a purchase, we may earn a small commission at no extra cost to you. Read our full Affiliate Disclosure.

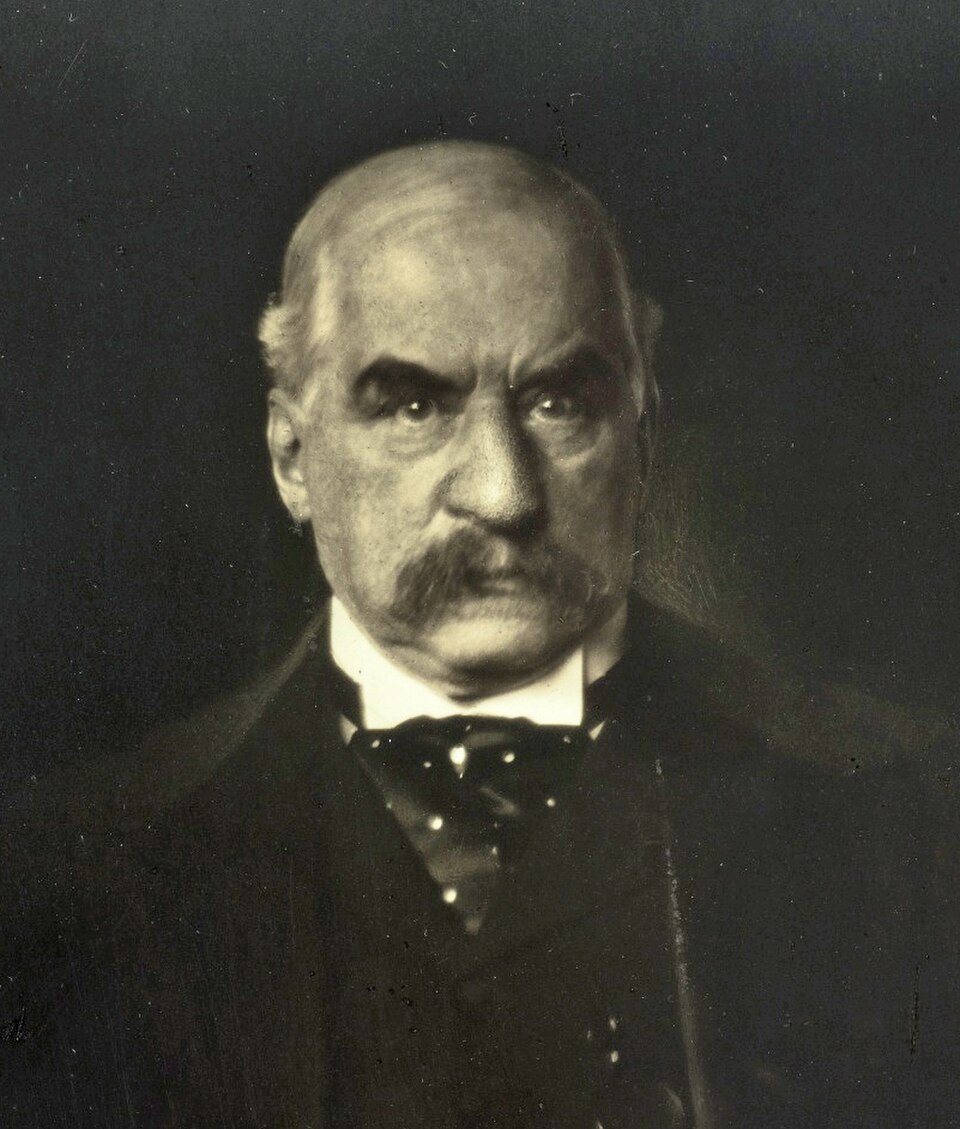

Some fortunes are built in calm weather. J.P. Morgan built his in storms.

When railroads were unstable, when the Treasury was strained, when markets panicked and the American financial system seemed ready to fracture, Morgan kept appearing at the center of the room. He was not just rich. He was where broken systems went to be reorganized.

That was the deeper source of his authority.

Morgan did not become one of the most feared men in American finance merely because he could write large checks. Plenty of rich men existed in the late 19th century. Morgan became different because he cultivated the ability to restore order when scale, complexity, and panic overwhelmed weaker institutions. He looked at disorder and saw a fee, a board seat, a controlling interest, and sometimes an entire new industrial architecture.

His story is not just a biography of a banker. It is the story of what happens when a fast-growing country relies on private power to keep the machine from flying apart.

The World Before the Fortune

Late 19th-century America was scaling faster than its institutions. Railroads sprawled. Industry consolidated. Capital rushed. But the structures needed to stabilize that growth were still incomplete. This created the ideal environment for a private organizer with money, contacts, and authority.

The country had size, energy, and ambition. It did not yet have fully mature mechanisms for managing nationwide industrial complexity. Financial markets were expanding, but they were often brittle. Corporate governance was loose. Railroad competition could become self-destructive. Public institutions lacked the modern central-bank-like tools that later generations would take for granted. In short, America had become large before it had become orderly.

That gap is where Morgan thrived.

Born in 1837, the son of financier Junius Spencer Morgan, he inherited access to elite financial circuits rather than inventing them from scratch. But inheritance alone does not explain what he became. Many men receive access. Fewer learn how to convert access into institutional command.

Morgan’s early ties to the Peabody network and the London financial world gave him two advantages that mattered enormously in the United States of his era. First, he had capital relationships that stretched beyond one city or one market. Second, he understood that American growth needed organization as much as it needed enthusiasm.

That insight would become the core of his empire.

It also gave him a psychological advantage over men who confused expansion with health. Morgan had fewer illusions about the cost of disorder. He knew that a rapidly growing system can look triumphant while quietly weakening underneath. That instinct made him unusually effective in sectors where everyone else wanted upside but nobody wanted to pay the price of coordination until a crisis made the bill impossible to ignore.

The Rise

Morgan’s early connections to transatlantic finance gave him access to capital and credibility. He reorganized railroads, stabilized financial bases, and increasingly became a director or influence center within the very systems he repaired.

Railroads were the perfect training ground because they were both indispensable and chaotic. They tied together national expansion, regional competition, freight pricing, industrial supply chains, and investor speculation. They were the arteries of the country, but many were overbuilt, badly managed, and financially unstable.

Morgan recognized that railroad disorder created a premium for someone who could impose discipline. He worked to stabilize finances, curb destructive competition, and reorganize capital structures. This was not glamorous work in the public sense. It was power in its most financial form.

By the 1880s and 1890s, he had extended influence across major lines and developed a reputation that made him increasingly unavoidable. Companies in distress, investors looking for confidence, and political actors fearing systemic disorder all learned the same lesson: when institutions became too large and too unstable, Morgan often ended up in the middle.

That position made him far more dangerous than a simple lender.

He was becoming an organizer of industrial America.

The Expansion of Power

His influence widened through railroads and then through industrial consolidations. He financed the creation of General Electric, helped assemble U.S. Steel, and coordinated major corporate structures. In 1895 he helped replenish the U.S. government’s gold reserve. In 1907 he led the private rescue effort that helped avert broader collapse.

Each of those episodes reveals the same pattern in a different costume.

With railroads, Morgan imposed rationalization where ruinous competition had been destroying value. With industrial combinations, he helped convert scattered enterprises into concentrated structures that investors could understand and governments could not easily ignore. General Electric and U.S. Steel were not just large corporations. They were signs that finance had become architecture.

The 1895 Treasury rescue demonstrated the same logic at sovereign scale. The U.S. government’s gold reserve was depleted, confidence was fraying, and Morgan assembled the syndicate that resupplied the reserve. This was not a minor episode in the history of influence. It was a moment when the federal government itself leaned on private financial power for stabilization.

Then came 1907, the event that permanently burned Morgan’s image into the mythology of American capitalism.

When panic hit and credit markets shook, Morgan gathered financiers, directed deposits, coordinated relief, and decided where private rescue capital would go. This is why so many later writers describe him as a kind of emergency central bank before the United States had one. He did not merely survive the panic. He acted as a command center inside it.

That role earned admiration, fear, and political backlash in equal measure.

Morgan’s great expansion, then, was not just expansion of wealth. It was expansion of jurisdiction. More and more sectors of American life seemed to become understandable only after they had passed through his hands.

That accumulation of jurisdiction is what turned him from a successful banker into a historical force. Each rescue widened his reach. Each reorganization expanded his network. Each demonstration of control made the next intervention easier because the market had already learned where authority seemed to reside.

The Hidden Strategy Behind the Fortune

Morgan’s hidden strategy was simple and devastating: become indispensable whenever scale outruns order.

He did not need to invent every enterprise. He needed to be the man who could make enterprises legible, stable, and financeable. In markets full of chaos, order itself became a premium service.

That is the key to understanding why Morgan mattered so much.

He was not trying to be the most romantic entrepreneur of the era. He was trying to be the man large systems needed once they grew too messy for ordinary management. He understood that disorder increases the value of coordination, and that whoever supplies coordination can end up extracting influence far beyond the original transaction.

This is what made his reorganization work so profitable. A railroad in trouble was not merely a distressed asset. It was a gateway. Stabilize the company, reshape the board, influence the pricing environment, connect it to capital, and suddenly the rescuer is no longer an outsider. He is part of the governing mechanism.

Morgan kept repeating this move.

He did it in transportation. He did it in industrial combinations. He did it in public credit episodes. He did it in panic management. Over time, the pattern itself became his empire.

The hidden strategy was not “be rich enough to intervene.” It was “make intervention itself the business.”

That distinction matters because it translates beautifully into modern business language. Some firms make products. Some make markets. Some stabilize systems that other people cannot keep stable themselves. The further up that hierarchy a firm moves, the more expensive and difficult it becomes to replace.

Morgan operated near the top of that ladder.

He sold confidence where confidence had become scarce. He sold reorganization where fragmentation had become destructive. He sold legitimacy to capital markets that wanted fewer surprises. The man himself became a kind of private institutional guarantee, and that was worth more than any single operating asset.

The Cost, Risk, or Backlash

The concentration of power around Morgan triggered distrust, reform pressure, and public anxiety. If one banker could shape so much of the American economy, the deeper question was whether the system itself was too dependent on private power.

That question did not emerge from nowhere.

To many observers, Morgan looked less like a financier and more like a private governor of capitalism. He sat on boards, influenced credit flows, helped assemble giant corporate combinations, and repeatedly appeared during national financial stress. Reformers and muckrakers saw in him a warning: if markets kept centralizing power in a handful of private hands, then democracy itself might end up trailing behind finance rather than supervising it.

In that sense, Morgan’s success helped create the demand for the very institutional reforms that would later reduce the need for a figure like him. The modern regulatory and central banking state did not appear in spite of Morgan’s era. In part, it appeared because the Morgan era made the risks of concentrated private stabilization impossible to ignore.

That is the paradox of his legacy.

He proved that private coordination could save a system from collapse. He also proved that no modern economy should be comfortable needing one man to do it.

Read The House of Morgan by Ron Chernow

The House of Morgan is a panoramic story of four generations in the powerful Morgan family and their secretive firms that would transform the modern financial world.

![House of Morgan (REV 10) by Chernow, Ron [Paperback (2010)]](https://m.media-amazon.com/images/I/31SI3uU1S-L.jpg)

Lessons for Modern Business Readers

1. Reorganization is a business model

Morgan shows that fixing broken systems can be more profitable than starting clean ones. Distress creates openings for whoever can restore structure.

2. Crisis creates authority for whoever can stabilize complexity

When panic hits, people stop rewarding noise and start rewarding reliability. The operator who can simplify a complex emergency often becomes the most powerful person in the room.

3. Capital plus judgment is more powerful than capital alone

Money without judgment is just weight. Morgan’s real edge was deciding which institutions deserved rescue, how to impose terms, and how to extract enduring influence from temporary instability.

4. System-level influence invites political backlash

The more indispensable a private actor becomes, the more likely the surrounding society will eventually question whether so much power should remain private.

5. Order is a premium product

In unstable markets, the ability to make institutions legible, financeable, and governable becomes one of the highest-value services in capitalism.

6. Great fortunes often form in the gap between growth and governance

Morgan’s life is a reminder that when an economy expands faster than its institutions, someone will make a fortune by organizing the chaos.

That lesson remains one of the most durable in finance. The largest opportunities often appear not where the market is clean and efficient, but where reality has become too complex for ordinary institutions to manage smoothly.

Book Recommendation

For the definitive follow-up, read The House of Morgan by Ron Chernow on Amazon.