A railroad war is never only about the rails. When Edward H. Harriman and James J. Hill collided over control of the Northern Pacific in 1901, the dispute forced Wall Street to choose sides in a way that almost no previous corporate rivalry had. The stock of a single railroad company rose from $150 to over $1,000 in a single morning before the market broke under the pressure. Fortunes were destroyed in minutes. Fortunes were also made.

Hidden Fortunes is interested in what sits below the surface of that drama. The real subject is how route control, financial alignment, and the capital market’s power to select which empire receives oxygen became the structural mechanism behind both men’s advantages. That mechanism is what this article is here to explain.

The World Before the Fortune

By the time Harriman and Hill were competing for dominance, American railroads had passed through two distinct phases. The first was construction — the era when grants of land and government capital made transcontinental routes possible and turned their builders into the first industrial aristocracy. The second was reorganization — the painful post-1893 period when bankrupt railroads were absorbed, restructured, and consolidated by bankers and operators who understood that route control mattered more than any single line’s operating margin.

The railway mania that built Britain’s infrastructure empire showed what speculative capital looked like when it chased railroad expansion without discipline. The American experience of the 1890s showed what happened after that discipline was imposed by financial necessity: the surviving operators were not the builders, but the consolidators.

Harriman entered that environment as a financier who understood how to use the reorganization process as a mechanism for control. Hill entered it as a builder who had never needed a government land grant to construct the Great Northern and understood, better than almost anyone, how operational efficiency compounded into strategic leverage over time. Their collision was not accidental. It was the inevitable result of two incompatible visions of what railroad empire actually meant.

The Rise

Harriman’s rise was built on the Union Pacific. He acquired control of it in 1897 when the railroad was emerging from bankruptcy and most investors considered it a wreck. He immediately invested $25 million in capital improvements, cut operating costs, and turned a reorganization project into one of the most profitable railroads in the country. The method was disciplined financial engineering applied to physical infrastructure — and it worked so consistently that Harriman began applying it to every line he could acquire.

The Erie War had shown what railroad rivalry looked like when it was conducted purely through financial manipulation — stock dilution, legal injunctions, and legislative capture. Harriman operated differently. He used genuine operational improvement as the foundation and financial control as the amplifier. By 1901 he controlled or influenced enough of the railroad network that observers began to speak of a single Harriman system spanning the continent.

Hill had taken a different path. He built the Great Northern without federal land grants, financing each segment from the operating profits of the previous one. That discipline forced him to understand terrain, freight economics, and regional development in ways that purely financial operators never did. His routes were built where traffic actually existed or could be created, not where subsidies made construction temporarily attractive. The result was a railroad that proved extraordinarily durable because it was designed from operational reality rather than capital-market opportunity.

The Expansion of Power

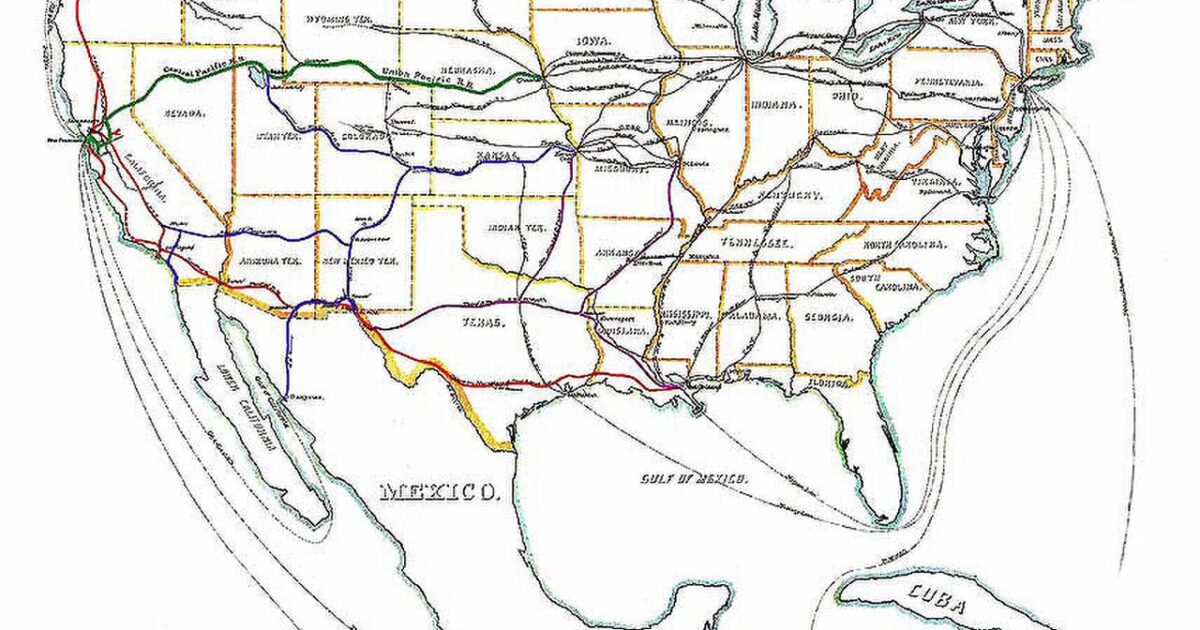

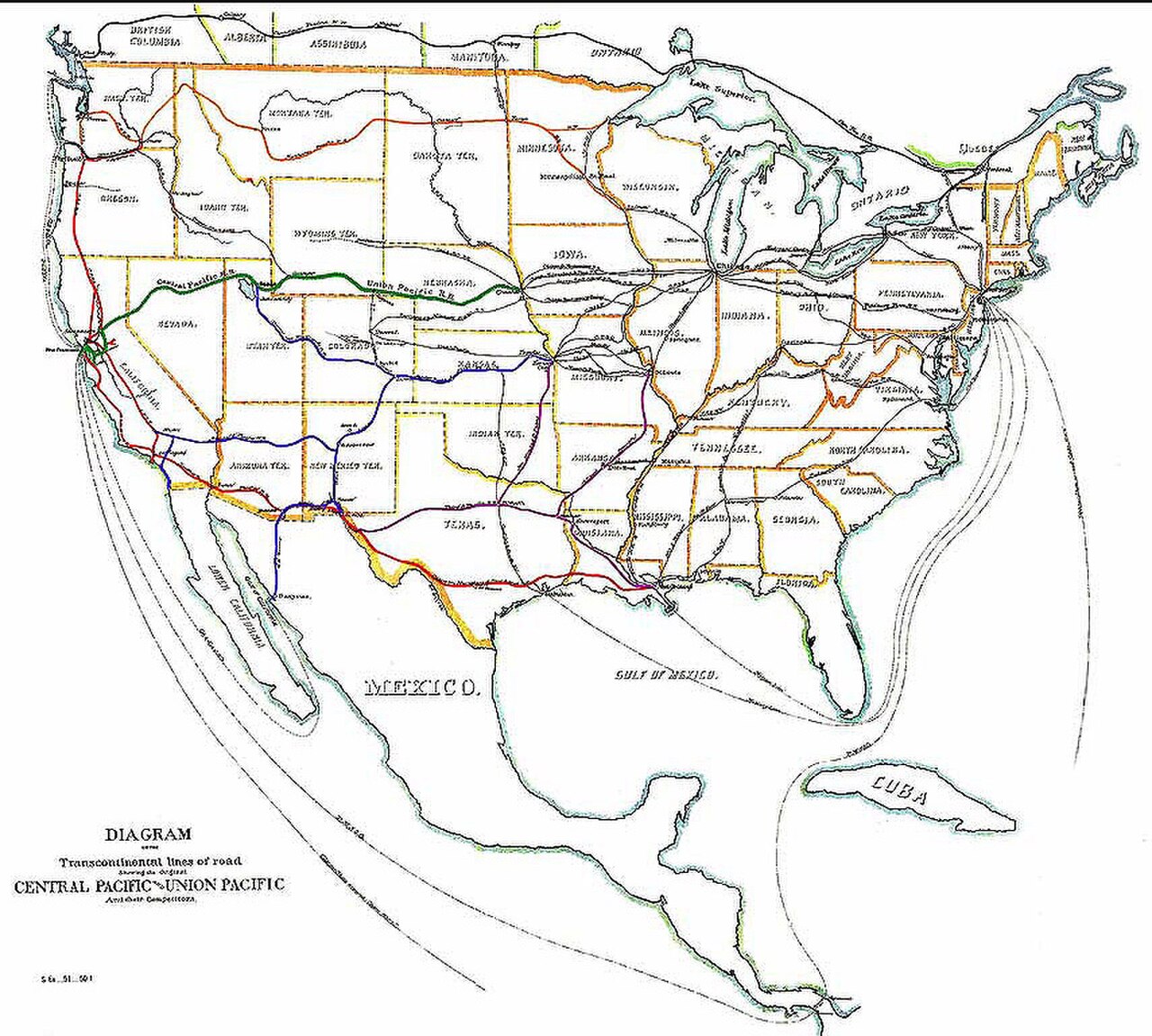

The collision point was the Burlington. The Chicago, Burlington and Quincy Railroad was the missing link that both men needed to complete their transcontinental strategies. It connected the northern routes to Chicago and the broader Midwest network, and whoever controlled it would have decisive leverage over freight flows across the entire northern tier of the country. Hill acquired it in 1901 in partnership with J.P. Morgan. Harriman attempted to buy it and was refused.

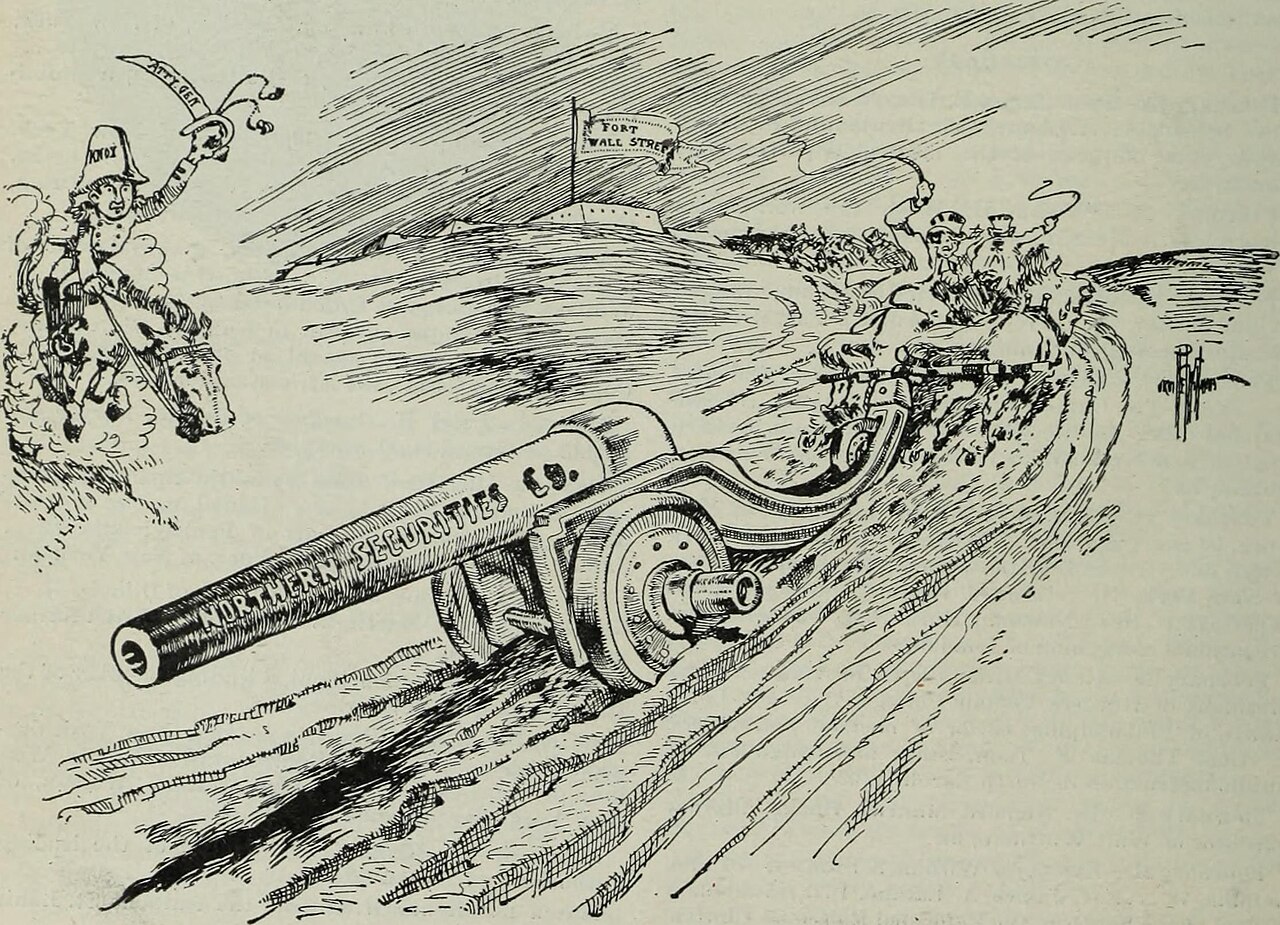

Harriman’s response was to buy control of the Northern Pacific — Hill’s gateway railroad — directly through the open market. He and his bankers began purchasing shares quietly in the spring of 1901, accumulating enough stock to potentially displace Hill’s board majority. Hill and Morgan countered by buying their own shares. J.P. Morgan’s ability to mobilize capital at speed was the decisive factor — the partnership stabilized the Northern Pacific position just as Harriman came close to majority control.

The market consequences of this fight were spectacular and destructive. Both sides were buying Northern Pacific stock simultaneously, and other investors who had sold short — betting the price would fall — found themselves unable to cover their positions at any rational price. The stock went vertical. Bystanders who had taken short positions lost everything. The episode became known as the Northern Pacific Corner of 1901, and it demonstrated that a purely financial struggle for railroad control could destroy unrelated market participants who had no stake in the underlying contest.

The Hidden Strategy Behind the Fortune

The hidden strategy behind both fortunes was the same in structure even if different in execution: control the route that everyone else still needs, and extract margin from that dependency indefinitely. Carnegie had done this with raw material supply. Rockefeller had done it with pipeline access. Harriman and Hill were doing it with the geographic chokepoints that determined where American freight could move efficiently and where it could not.

The resolution of the 1901 confrontation was the Northern Securities Company — a holding company created by Hill and Morgan to consolidate the Northern Pacific, the Great Northern, and the Burlington under a single legal entity, removing them from the competitive market permanently. It was an elegant financial solution to a destructive rivalry, and it was also an immediate target for the new administration of Theodore Roosevelt, who used it as the first major test of antitrust enforcement under the Sherman Act.

The deeper lesson for Hidden Fortunes readers is that both men understood their real asset was not the railroad but the route. The route was what made shippers dependent, what gave them leverage over connecting lines, and what produced the freight pricing power that turned operational margins into permanent advantage. The physical infrastructure was the evidence of control, but the control itself was geographic and logistical — the kind of advantage that competitors cannot easily replicate because geography does not change on demand.

The Cost, Risk, or Collapse

The Northern Pacific Corner demonstrated what happens when financial rivalry overrides market function. The short sellers who were destroyed in May 1901 had nothing to do with the Harriman-Hill contest — they were simply participants in a liquid market who found that liquidity had been removed by two competing principals who needed the same shares. Their losses were real and total, and neither Harriman nor Hill bore any responsibility for them under the law as it then stood.

The antitrust dissolution of Northern Securities in 1904 forced a different kind of reckoning. The Supreme Court ruled five to four that the holding company violated the Sherman Act, and the railroads were required to separate. The practical effect was limited — Hill and Harriman both retained their individual railroad positions, and the competitive dynamics of the northern routes did not fundamentally change. But the legal precedent was significant. It established that financial consolidation of competing railroads could not proceed indefinitely without regulatory constraint, and it set the terms for the next forty years of railroad regulation.

Harriman died in 1909, still at the height of his influence but facing mounting political and regulatory hostility. Hill survived until 1916, long enough to see the railroad industry begin its decline relative to the automobile and the highway. Both men built systems that were genuinely excellent by the standards of their era, and both men built them in ways that concentrated power so completely that the political system eventually had to respond.

Lessons for Modern Business Readers

1. Route control beats asset ownership

Harriman and Hill both understood that owning the physical railroad mattered less than controlling the route that competitors and shippers could not avoid. The geographic chokepoint — not the locomotive or the track — was the actual source of leverage. Modern equivalents appear everywhere that infrastructure creates mandatory dependency.

2. Financial rivalry can destroy unrelated participants

The Northern Pacific Corner of 1901 imposed catastrophic losses on market participants who had no involvement in the Harriman-Hill contest. When two well-capitalized principals compete for the same scarce asset, the collateral damage can extend far beyond the principals themselves. This pattern recurs in every era where financial markets intersect with infrastructure control.

3. Consolidation invites regulatory response

The Northern Securities Company was a rational financial solution to a destructive rivalry, and it was immediately targeted by the Roosevelt administration precisely because it was effective. Power concentrated enough to eliminate market competition will eventually attract legal constraint. The timing and severity of that constraint are uncertain; its eventual arrival is not.

4. Operational excellence and financial control compound differently

Hill built from operations outward. Harriman built from financial control inward. Both methods produced formidable positions, but Hill’s approach created infrastructure that was genuinely superior for its purpose, while Harriman’s approach maximized financial returns from existing assets. The comparison illustrates that there are multiple valid architectures for building durable competitive advantage.

5. Capital speed is a strategic weapon

The Northern Securities case showed that whoever could mobilize capital faster than a rival could determine the outcome of a control contest before the rival could respond. Morgan’s ability to deploy capital in hours rather than days was not merely a financial capability — it was a strategic weapon that decided the 1901 confrontation.

6. The arbitrator often captures value from the combatants

J.P. Morgan brokered the Northern Securities solution after helping Hill win the stock battle. In both roles he extracted fees, relationships, and influence from a conflict he did not initiate but helped resolve. The arbitrator who can end a destructive rivalry often captures more durable value than either principal, because the principals are exhausted and the arbitrator remains intact.